Ever look at your bank account at the end of the month and wonder where it all went? I've been there. Living on a tight income isn't just about pinching pennies — it's about making smarter choices every single day. And the good news? You don't need a six-figure salary to get ahead financially.

I've spent years studying personal finance, and I'm here to tell you: learning to live on a low income is one of the most powerful money skills you can build. These 40 hacks will help you stretch every dollar, cut unnecessary spending, avoid financial pitfalls, and — yes — even start saving and investing on a shoestring budget.

Let's dive in.

What Does "Living on a Low Income" Actually Mean?

Before we get into the hacks, let's get real about what we're dealing with. Living on a low income isn't just a matter of earning less — it's about managing what you have with intention. Whether you're making $25,000 a year or $60,000 in a high-cost city, these principles apply.

Key Terms to Know:

Discretionary Income — The money left over after paying for necessities like rent, food, and utilities. This is your financial breathing room.

Fixed Expenses — Bills that stay the same each month (rent, loan payments, insurance).

Variable Expenses — Costs that change month to month (groceries, dining out, entertainment).

Zero-Based Budgeting — A system where every single dollar has a job. Income minus expenses equals zero — not because you're broke, but because everything is allocated.

Lifestyle Inflation — The sneaky habit of spending more as you earn more. It's the #1 wealth killer.

Emergency Fund — A dedicated savings buffer (typically 3–6 months of expenses) to cover unexpected costs without going into debt.

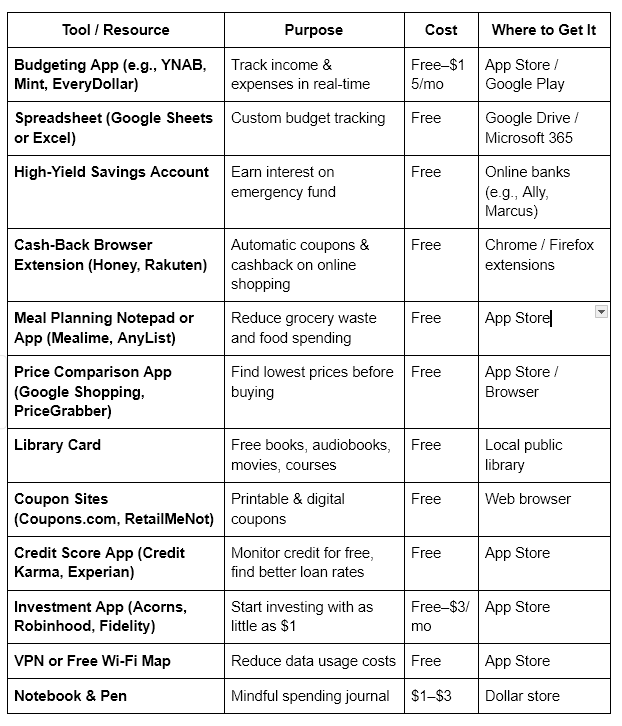

Materials Needed: Your Low-Income Survival Toolkit

You don't need expensive software or a financial advisor to get started. Here's everything you need, most of it free:

The 40 Hacks: Broken Down by Category

💰 Budget & Money Mindset (Hacks 1–8)

1. Build a Zero-Based Budget — Every. Single. Month.

I know "budget" sounds boring. But here's the thing: a budget isn't a restriction. It's permission to spend guilt-free in the right places. Zero-based budgeting means you assign every dollar a purpose before the month starts. Apps like YNAB (You Need a Budget) make this painless. People who use a written budget save an average of $200 more per month than those who don't.

2. Automate Your Savings the Day You Get Paid

Don't wait to "see what's left." Pay yourself first. Set up an automatic transfer to a savings account the moment your paycheck lands. Even $25 a week adds up to $1,300 a year. You won't miss what you never see.

3. Use the 50/30/20 Rule as Your Starting Framework

50% — Needs (rent, food, utilities, transportation)

30% — Wants (dining out, subscriptions, entertainment)

20% — Savings & debt repayment

If your income is very tight, flip it to 70/20/10 temporarily. The key is having a framework, not a perfect one.

4. Apply the 30-Day Rule Before Big Purchases

Want to buy something over $50? Write it down. Wait 30 days. If you still want it after a month, buy it. More often than not, the urge passes — and you keep your money.

5. Do a Monthly "Financial Date" With Yourself

Sit down once a month, cup of tea in hand, and review your budget. Where did you overspend? Where did you do great? Awareness alone can change behavior. People who track their spending regularly reduce impulse purchases by up to 30%.

6. Ditch the "Treat Yourself" Trap

I'm not saying never enjoy anything. But "I deserve this" is the most dangerous phrase in personal finance. Every unnecessary purchase is a future bill. Reframe it: "I deserve financial freedom more than I deserve this right now."

7. Build an Emergency Fund Before Everything Else

Debt is a wealth vacuum. The best way to avoid new debt is to have a cash buffer. Start with a $1,000 mini-emergency fund, then build to 3 months of expenses. Keep it in a high-yield savings account earning 4–5% APY (as of 2024–2025).

8. Know Your "Hourly Cost of Life"

Divide your monthly expenses by the hours you work each month. If you work 160 hours and spend $3,200/month, every hour of your life costs $20. Now ask: is that $80 dinner worth 4 hours of your life? This reframe is genuinely transformative.

Grocery & Food Hacks (Hacks 9–16)

9. Meal Plan Every Week — No Exceptions

Unplanned dinners are expensive dinners. Spend 20 minutes each Sunday planning 7 dinners, writing a precise grocery list, and sticking to it. Families who meal plan spend 25–30% less on groceries.

10. Shop Grocery Store Perimeters First

Fresh produce, proteins, and dairy live on the outer edges. The middle aisles are where processed, overpriced temptations live. Do a perimeter pass first, then — only if needed — dip into the aisles.

11. Buy In Bulk Strategically (Not Blindly)

Bulk buying only saves money if you use everything before it expires. Dry goods (rice, lentils, oats, pasta), canned goods, and cleaning supplies are bulk-buy champions. Fresh produce, often not.

12. Eat Leftovers Like a Pro

Cook once, eat twice. Double your dinner recipe and have lunch sorted for the next day. Americans throw away roughly $1,500 worth of food per year — don't be that statistic.

13. Own-Brand Is Almost Always Fine

Supermarket own-brand products cost 20–40% less than name brands. For staples like flour, canned tomatoes, pasta, rice, and cleaning products, there's zero quality difference. Stop paying for the label.

14. Grow Your Own — Even in an Apartment

Herbs like basil, mint, and chives grow in windowsill pots for a one-time cost of $2–3 per plant. Tomatoes, peppers, and lettuce grow in small containers on balconies. Fresh herbs at the grocery store run $3–5 per bundle — growing your own pays off in weeks.

15. Use Cashback and Coupon Apps at the Checkout

Apps like Ibotta, Fetch Rewards, and Flipp give you real cashback on grocery purchases. Ibotta users save an average of $240/year just by scanning receipts. Stack these with store sales for maximum savings.

16. Do a "Pantry Week" Once a Month

Once a month, challenge yourself to a no-shopping week. Use up what's already in your freezer, pantry, and fridge. You'll be shocked how many meals are already hiding in your kitchen — and you'll slash your grocery bill for that week to near zero.

Home & Utilities (Hacks 17–23)

17. Audit Your Subscriptions Ruthlessly

The average American spends over $200/month on subscriptions they've half-forgotten about. Go through your bank statements right now. Cancel anything you haven't used in the last 30 days. Tools like Rocket Money or Trim can automate this audit.

18. Unplug Electronics When Not in Use

"Phantom load" or standby power accounts for 5–10% of household electricity use. Unplugging TVs, game consoles, chargers, and appliances when idle can save $100–$200 a year. Power strips with switches make this effortless.

19. Switch to LED Bulbs Throughout Your Home

LED bulbs use 75% less energy than incandescent bulbs and last 15–25 times longer. Replacing 10 bulbs saves approximately $60–$80 per year on electricity alone. The upfront cost pays for itself in 3–6 months.

20. Wash Clothes in Cold Water

Modern detergents work just as effectively in cold water. About 90% of the energy used in washing clothes goes to heating the water. Switching to cold washes can cut laundry costs by 75% — saving $60–$150 a year depending on usage.

21. Lower Your Thermostat by 2 Degrees

Each degree you lower your heating in winter saves roughly 1–3% on your heating bill. A programmable or smart thermostat (Nest, Ecobee) pays for itself within a year. Set it lower at night and when you're out — you'll barely notice the difference.

22. Negotiate Your Bills — Every Single Year

Your internet, phone, and insurance providers don't want to lose you. Call them annually and ask for a loyalty discount or threaten to switch. 70% of people who call and ask for a lower rate get one. This one phone call can save $200–$600 a year.

23. Weatherproof Your Home for Cheap

Drafty windows and doors are money leaking out of your home. Door draft stoppers ($5–$10), weatherstripping tape ($8–$15), and window insulation film ($15–$25) can reduce heating/cooling costs by 10–15%. These are some of the highest-return small investments you can make.

Transportation (Hacks 24–27)

24. Keep Your Tires Properly Inflated

Under-inflated tires reduce fuel efficiency by 0.5–3% per PSI below optimal. Check your tire pressure monthly. It takes 5 minutes and costs nothing — and can save you $50–$150 in fuel annually.

25. Carpool or Use Rideshare Strategically

If commuting alone, find a colleague to share the ride. Splitting fuel and parking costs can cut commuting expenses in half. Apps like BlaBlaCar, Waze Carpool, or even a group text with coworkers can set this up in minutes.

26. Consider a Prepaid Phone Plan

Big carrier contracts lock you into paying $70–$100/month for service. MVNOs (Mobile Virtual Network Operators) like Mint Mobile, Visible, or Cricket offer the same coverage (they run on the same towers) for $15–$35/month. That's a $500–$800/year saving.

27. Combine Errands Into Single Trips

Every unnecessary car trip costs you in fuel. Plan your week so that errands — grocery store, pharmacy, post office — happen in a single loop. This simple habit can save 15–20 miles of driving per week.

Debt, Credit & Banking (Hacks 28–32)

28. Use the Debt Avalanche Method to Pay Off Debt Faster

List your debts from highest to lowest interest rate. Attack the highest-interest debt first while paying minimums on all others. Once it's gone, roll that payment into the next one. This method saves the most money in interest over time. (The debt snowball — smallest balance first — works better psychologically for some people. Pick what you'll actually stick to.)

29. Never Pay a Bank Fee Again

Monthly maintenance fees, overdraft fees, ATM fees — these are optional charges most people don't realize they can avoid. Switch to a free checking account (Chime, Ally, Capital One 360) and set up low-balance alerts. Bank fees can add up to $200–$400 a year without people even noticing.

30. Use Cashback Credit Cards (And Pay Them in Full)

If you have the discipline to pay your balance in full every month, a cashback credit card is free money. Cards like the Citi Double Cash (2% on everything) or Discover it (5% rotating categories) put real cash back in your pocket. The critical rule: never carry a balance. Interest charges will always cancel out cashback benefits.

31. Check and Improve Your Credit Score

A higher credit score means lower interest rates on loans, mortgages, and credit cards. Use a free service like Credit Karma to monitor your score. Pay bills on time, keep credit utilization below 30%, and don't close old accounts. Even improving your score by 50 points can save thousands on a mortgage.

32. Avoid Payday Loans at All Costs

Payday loans charge APRs of 300–400%. They're debt traps dressed as quick solutions. If you're in a cash crunch, look for local credit union emergency loans, employer advances, or community assistance programs first.

Side Income & Wealth Building (Hacks 33–40)

33. Start a Side Hustle That Fits Your Schedule

You don't need to quit your job. Even $200–$500 extra per month changes your financial picture dramatically. Ideas include:

Freelance writing, design, or coding on Fiverr or Upwork

Selling items on eBay, Facebook Marketplace, or Vinted

Tutoring or teaching English online

Dog walking or pet sitting via Rover

Delivering groceries with Instacart or Shipt

34. Sell What You're Not Using

Do a ruthless declutter. Unused electronics, clothes, furniture, books — all of it has value. One good eBay or Facebook Marketplace session can generate $200–$1,000+ and reclaim space in your home. Use that cash to pay down debt or seed your emergency fund.

35. Invest — Even When You Think You Can't

You don't need thousands of dollars to start investing. Apps like Acorns round up your purchases and invest the spare change. Fidelity and Schwab offer zero-minimum index funds. Even $50/month invested consistently over 30 years grows to over $85,000 at a 7% average return. Time is your biggest asset.

36. Maximize Every Free Work Benefit

If your employer offers a 401(k) match, contribute at least enough to get the full match. This is a 100% return on that portion of your money — no investment in the world beats it. Also maximize any HSA, FSA, or employee assistance programs available to you.

37. Use Your Library Card Like a Subscription Service

A library card unlocks free e-books, audiobooks (Libby/OverDrive), streaming services (Kanopy, hoopla), magazines, online courses (LinkedIn Learning at many libraries), and even museum passes. This one card can replace $50–$100/month in subscriptions.

38. Shop Sales with Intention

Major sales events (Black Friday, Labor Day, end-of-season clearance) offer genuine discounts on quality items — but only if you're buying something you actually need. Make a wish list in advance. Buy what's on it at a discount. Avoid buying things just because they're on sale.

39. Learn One New Money Skill Per Month

Read one personal finance book, take one free online course, or listen to one podcast per month. Knowledge compounds just like money. Resources like The Total Money Makeover by Dave Ramsey, I Will Teach You to Be Rich by Ramit Sethi, or the "Bigger Pockets Money" podcast are excellent starting points.

40. Plan for Retirement — Even on a Tight Budget

It feels impossible when money is tight, but even $25/month in a Roth IRA matters. The tax-free growth over decades is remarkable. At $25/month starting at age 25, with 7% average returns, you'd have over $65,000 by age 65. Start tiny. Start now.

Tips for Success

Automate everything you can. Automation removes willpower from the equation. Savings, bill payments, and investments should all happen without you having to remember.

Track your spending weekly, not just monthly. Monthly reviews are great, but weekly check-ins catch problems early.

Celebrate small wins. Paid off a credit card? Emergency fund hit $500? Celebrate it. Progress motivation is real.

Find an accountability partner. Tell a trusted friend your financial goals. People with accountability partners are significantly more likely to reach their goals.

Stop comparing yourself to others. Social comparison spending is a silent wealth killer. Your neighbor's lifestyle may be funded by debt you don't see.

Review your budget when life changes. New job, new city, new baby — every life change deserves a budget reset.

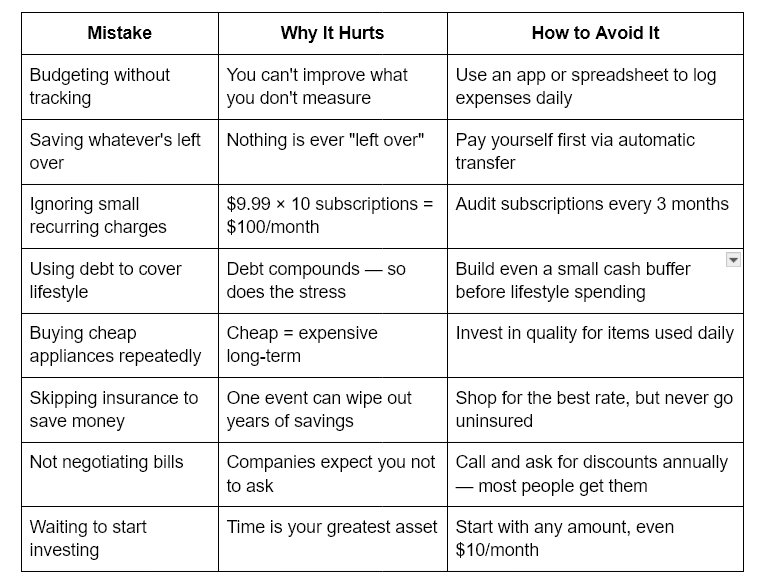

Common Mistakes and How to Avoid Them

Similar Strategies Worth Exploring

These approaches pair naturally with the hacks above:

The No-Spend Challenge — Pick a weekend, a week, or a full month and commit to zero discretionary spending. Use it to reset spending habits and pad savings.

Envelope Budgeting — Physically separate cash into envelopes labeled for each spending category. When the envelope is empty, spending in that category stops.

The Frugal Living Movement — A broader lifestyle philosophy focused on intentional spending, DIY skills, and valuing experiences over things. Communities like r/Frugal on Reddit are rich with practical ideas.

Geo-Arbitrage — Living in a lower cost-of-living city while earning a remote income pegged to a higher-cost market. One of the fastest ways to dramatically increase your savings rate.

Financial Independence / Retire Early (FIRE) — A movement focused on aggressively saving 50–70% of income to retire decades early. Even partial FIRE principles can dramatically improve your financial position.

Outro

Living on a low income isn't a life sentence — it's a starting point. Every single one of these 40 hacks is something I've either used personally or seen work for others. You don't need to implement all 40 at once. Pick five that feel achievable right now, commit to them for 30 days, and see what changes. Small, consistent actions are what separate people who struggle financially from those who thrive.

The most important truth in all of personal finance? You can live on a low income and still build wealth. It just requires more intention, more creativity, and a willingness to play the long game. Start today not next month, not when the salary goes up. Today. Your future self is counting on you.